Attorney-Approved Promissory Note Document

Attorney-Approved Promissory Note Document

When it comes to borrowing or lending money, a Promissory Note is an essential document that outlines the agreement between the two parties involved. This simple yet powerful tool serves as a written promise from the borrower to repay a specific amount of money to the lender, often within a set timeframe. The form typically includes key details such as the principal amount, interest rate, repayment schedule, and any penalties for late payments. Additionally, it may specify whether the loan is secured or unsecured, providing clarity on the lender's rights in case of default. By using a Promissory Note, both parties can establish clear expectations and protect their interests, making it a vital component of any lending arrangement. Understanding the nuances of this form can help individuals navigate financial transactions with confidence.

Promissory Note

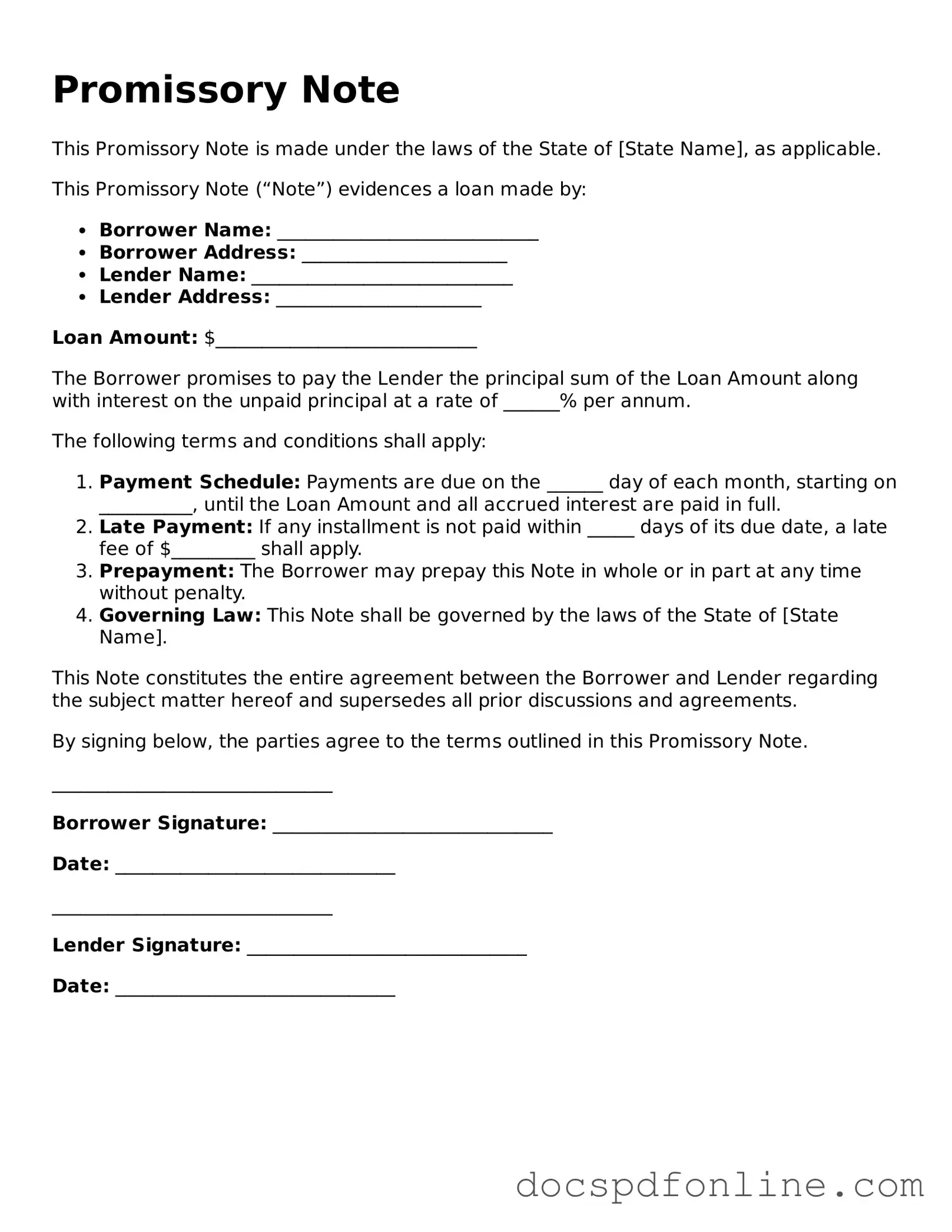

This Promissory Note is made under the laws of the State of [State Name], as applicable.

This Promissory Note (“Note”) evidences a loan made by:

Loan Amount: $____________________________

The Borrower promises to pay the Lender the principal sum of the Loan Amount along with interest on the unpaid principal at a rate of ______% per annum.

The following terms and conditions shall apply:

This Note constitutes the entire agreement between the Borrower and Lender regarding the subject matter hereof and supersedes all prior discussions and agreements.

By signing below, the parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower Signature: ______________________________

Date: ______________________________

______________________________

Lender Signature: ______________________________

Date: ______________________________

Incomplete Information: Many individuals fail to provide all necessary details. This includes missing names, addresses, or the date of the agreement. Ensure every section is filled out completely.

Incorrect Loan Amount: Double-check the loan amount. Some people either write the wrong figure or miscalculate the total. This can lead to disputes later on.

Missing Signatures: A common oversight is neglecting to sign the document. Both the borrower and lender must sign the note for it to be valid.

Not Specifying Interest Rates: Failing to include an interest rate can create confusion. Clearly state whether the loan is interest-free or if there are specific rates applied.

Ignoring Payment Terms: It's essential to outline the payment schedule. Specify due dates and the frequency of payments to avoid misunderstandings.

Vague Repayment Terms: Be clear about how the loan will be repaid. Include details on whether payments are made in installments or as a lump sum.

Failure to Include Collateral: If the loan is secured, be sure to describe the collateral. This protects the lender in case of default.

Not Consulting Legal Advice: Some individuals skip this step. Consulting with a legal professional can help ensure that the note is valid and enforceable.

Not Keeping Copies: After completing the form, it’s crucial to keep copies for both parties. This provides a reference in case any issues arise in the future.

How to Fill Out W9 - Using a W-9, businesses can report payments made to you to the IRS.

The California Release of Liability form is a legal document by which a person relinquishes their right to bring a lawsuit against another party for any injuries or damages suffered. This agreement is often used in situations where individuals participate in potentially hazardous activities or events. For more information on how to properly execute this form and avoid any ambiguities, you can visit TopTemplates.info. It serves as a crucial tool in managing legal risks and providing peace of mind for both parties involved.

Usda 7001 - The form should be stamped or include the veterinarian's name and address.

Annual Physical Basic Physical Exam Form Pdf - Indicate whether hearing screening results warrant specialist referral.

When filling out a Promissory Note form, it's essential to ensure accuracy and clarity. Here are some guidelines to follow:

Understanding the Promissory Note form can be challenging, and several misconceptions often arise. Here’s a list of ten common misunderstandings about this important financial document.

By addressing these misconceptions, individuals can better understand the role and importance of promissory notes in financial transactions.

Once you have the Promissory Note form in front of you, it's time to fill it out carefully. Make sure you have all the necessary information at hand, as accuracy is crucial. Follow these steps to complete the form correctly.

After completing the form, review it thoroughly to ensure all information is accurate and complete. Once finalized, both parties should keep a copy for their records.