Fill Your Profit And Loss Form

Fill Your Profit And Loss Form

The Profit and Loss form serves as a crucial financial document for businesses of all sizes. This form provides a clear snapshot of a company's revenues, costs, and expenses over a specific period. By summarizing income and expenditures, it helps business owners understand their financial performance. The form typically includes sections for sales revenue, cost of goods sold, gross profit, operating expenses, and net profit or loss. Each section allows for a detailed breakdown, enabling businesses to identify trends, manage budgets, and make informed decisions. Analyzing the Profit and Loss form can reveal areas of strength and weakness, guiding strategic planning. Understanding this form is essential for anyone looking to grasp the financial health of a business, whether they are entrepreneurs, investors, or stakeholders.

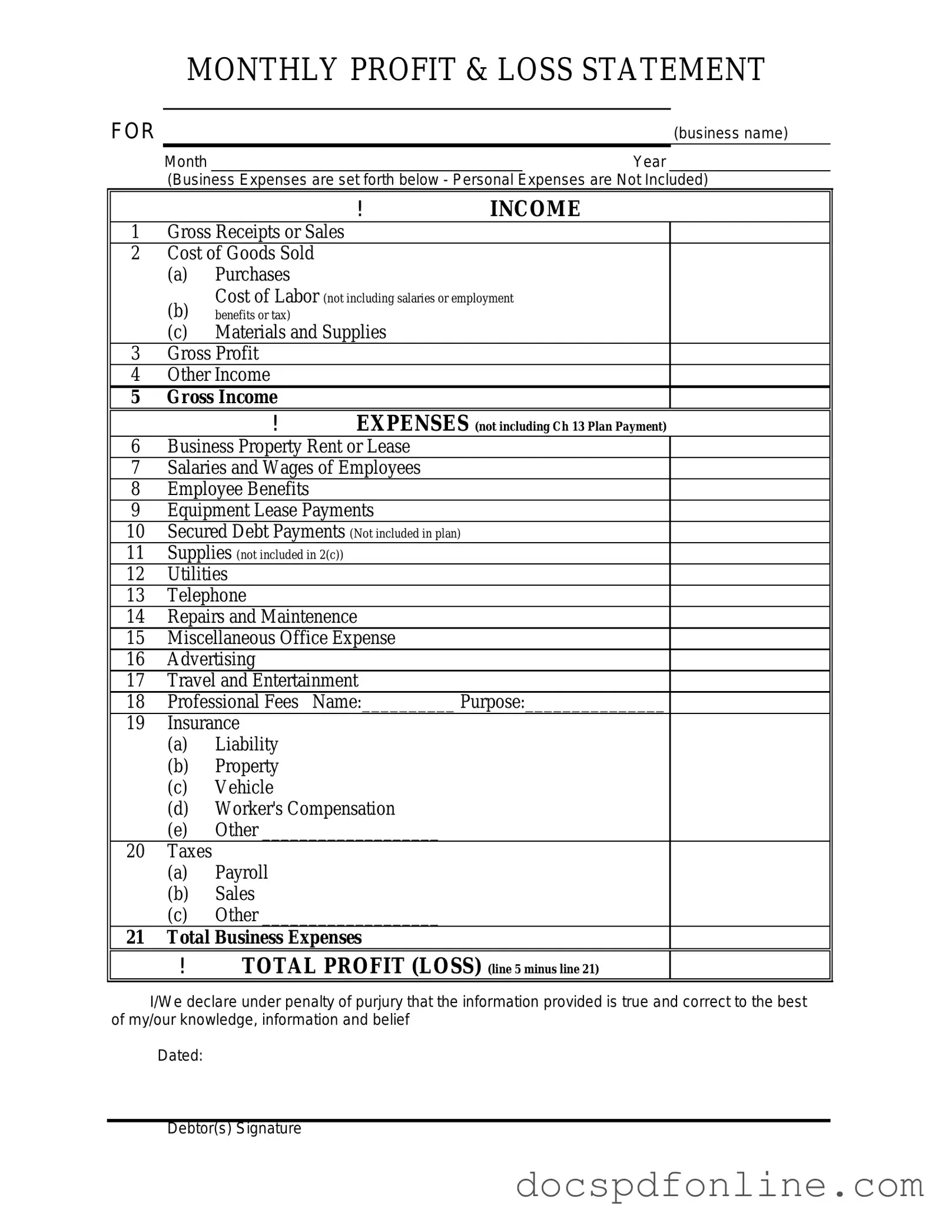

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

Neglecting to include all income sources: Many individuals overlook secondary income streams, such as freelance work or side businesses. It is essential to account for every source of income to get an accurate picture of financial health.

Failing to categorize expenses correctly: Misclassifying expenses can lead to inaccurate profit calculations. Ensure that expenses are organized into appropriate categories, such as operational costs, marketing, and salaries.

Not updating figures regularly: Relying on outdated information can skew results. Regular updates to the Profit and Loss form are necessary to reflect the current financial situation accurately.

Ignoring one-time expenses: Some people forget to include irregular expenses that can significantly impact profitability. It’s important to factor in these costs to avoid misleading conclusions about financial performance.

Overlooking the importance of accuracy: Small mistakes in data entry can lead to major discrepancies. Double-checking figures and calculations is crucial to ensure the integrity of the Profit and Loss statement.

Time Card Example - Facilitates communication regarding hours with supervisors.

Hazmat Bol - It indicates the origin and destination zip codes for clarity in transport logistics.

In addition to the provided ADP Pay Stub form, employees seeking a convenient way to generate their pay stubs can utilize resources like My PDF Forms, which offers templates and tools for easily accessing and managing their financial documents.

Test Drive Agreement - The dealership will not cover any loss of personal property left inside the vehicle.

When filling out the Profit and Loss form, it's important to ensure accuracy and clarity. Here’s a list of things to do and avoid:

Understanding the Profit and Loss form is essential for anyone managing a business's finances. However, several misconceptions can lead to confusion. Here are four common misconceptions:

By addressing these misconceptions, business owners can better utilize the Profit and Loss form to enhance their financial management practices.

Filling out the Profit and Loss form is an important step in managing your business finances. Accurate completion of this form will help you track income and expenses, providing a clear picture of your financial health. Follow the steps below to ensure that you fill out the form correctly and efficiently.