Attorney-Approved Deed in Lieu of Foreclosure Document

Attorney-Approved Deed in Lieu of Foreclosure Document

When homeowners face financial difficulties and the threat of foreclosure looms, they often seek alternatives to protect their interests and minimize the impact on their credit scores. One such option is the Deed in Lieu of Foreclosure, a legal document that allows a homeowner to voluntarily transfer ownership of their property back to the lender. This process can be a more amicable solution than foreclosure, which can be lengthy and detrimental to a homeowner’s financial future. By signing the Deed in Lieu of Foreclosure, the homeowner typically relinquishes their rights to the property in exchange for the lender forgiving the remaining mortgage debt. This arrangement can streamline the process of exiting homeownership while providing the lender with a quicker resolution to recover their investment. However, it is essential to understand the implications of this decision, including potential tax consequences and the impact on credit ratings. Homeowners must also consider whether they are eligible for this option and what steps are necessary to initiate the process. Overall, the Deed in Lieu of Foreclosure can serve as a valuable tool for those navigating the challenges of homeownership in difficult financial times.

Deed in Lieu of Foreclosure Template

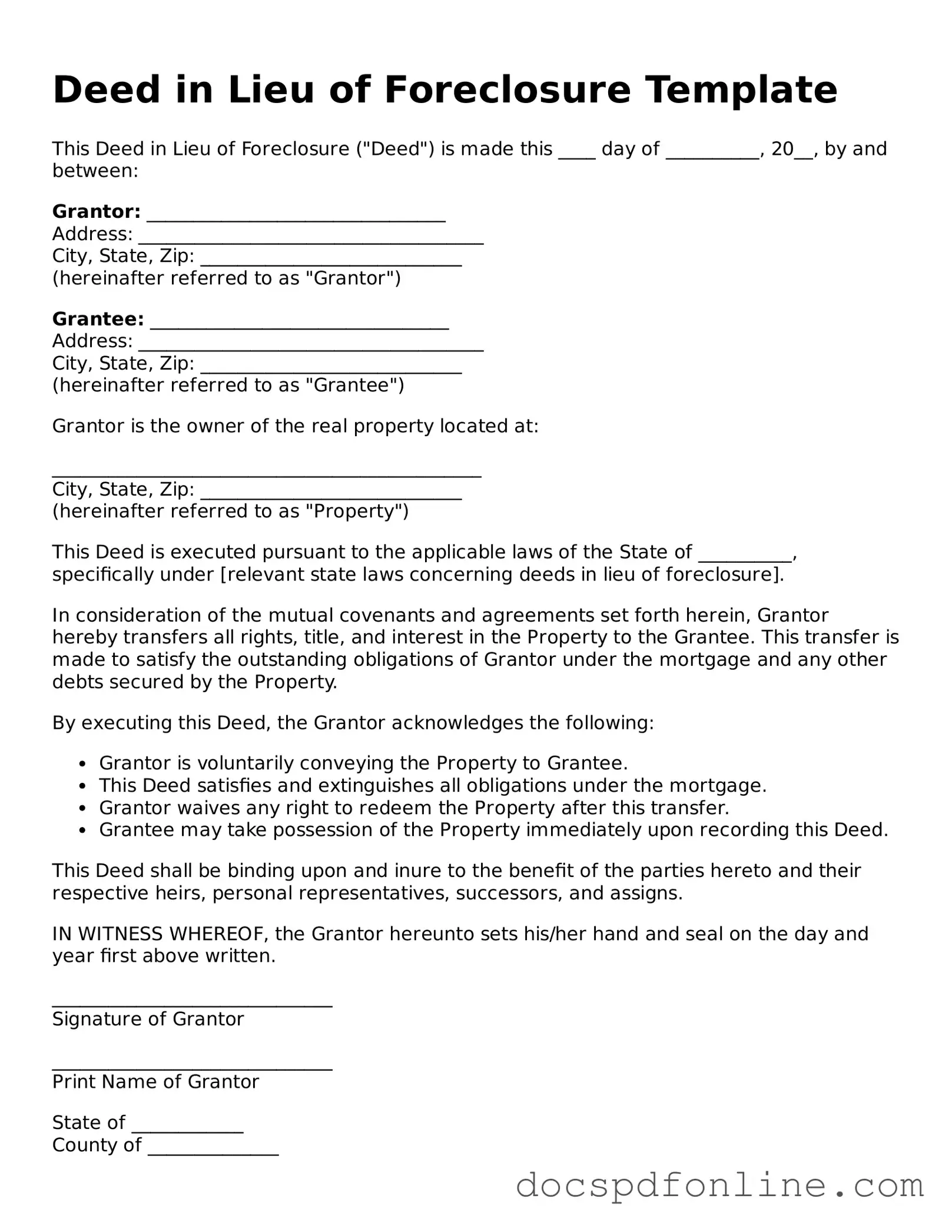

This Deed in Lieu of Foreclosure ("Deed") is made this ____ day of __________, 20__, by and between:

Grantor: ________________________________

Address: _____________________________________

City, State, Zip: ____________________________

(hereinafter referred to as "Grantor")

Grantee: ________________________________

Address: _____________________________________

City, State, Zip: ____________________________

(hereinafter referred to as "Grantee")

Grantor is the owner of the real property located at:

______________________________________________

City, State, Zip: ____________________________

(hereinafter referred to as "Property")

This Deed is executed pursuant to the applicable laws of the State of __________, specifically under [relevant state laws concerning deeds in lieu of foreclosure].

In consideration of the mutual covenants and agreements set forth herein, Grantor hereby transfers all rights, title, and interest in the Property to the Grantee. This transfer is made to satisfy the outstanding obligations of Grantor under the mortgage and any other debts secured by the Property.

By executing this Deed, the Grantor acknowledges the following:

This Deed shall be binding upon and inure to the benefit of the parties hereto and their respective heirs, personal representatives, successors, and assigns.

IN WITNESS WHEREOF, the Grantor hereunto sets his/her hand and seal on the day and year first above written.

______________________________

Signature of Grantor

______________________________

Print Name of Grantor

State of ____________

County of ______________

On this ____ day of __________, 20__, before me, a Notary Public in and for said county and state, personally appeared _____________________, who is known to me or satisfactorily proven to be the person whose name is subscribed to this instrument, and acknowledged that he/she executed the same for the purposes therein contained.

IN WITNESS WHEREOF, I have hereunto set my hand and official seal.

______________________________

Notary Public

My Commission Expires: ____________

Failing to understand the implications of a Deed in Lieu of Foreclosure. Many individuals do not fully grasp that this process involves transferring ownership of their property to the lender, which may have long-term effects on their credit and financial situation.

Not confirming the eligibility criteria. Some people overlook the specific requirements set by their lender, such as being current on mortgage payments or having a financial hardship.

Neglecting to consult with a legal or financial advisor. Seeking professional guidance can help clarify the process and ensure that the individual’s rights are protected.

Overlooking the need for a clear title. Individuals often forget to ensure that there are no additional liens or claims against the property, which can complicate the transfer.

Inadequately completing the form. Mistakes in filling out the form, such as incorrect names or property descriptions, can lead to delays or rejection of the deed.

Failing to provide necessary documentation. Many people do not attach required documents, such as proof of income or hardship letters, which can hinder the process.

Not understanding tax implications. Individuals may not realize that a Deed in Lieu could have tax consequences, such as potential liability for cancellation of debt income.

Rushing the process. Some individuals attempt to complete the deed too quickly without fully considering all aspects and implications, leading to oversight.

Ignoring the lender’s policies. Each lender may have unique requirements or processes for accepting a Deed in Lieu, and failing to adhere to these can result in complications.

Not keeping copies of submitted documents. Failing to maintain records of what was submitted can create issues if disputes arise later on.

California Correction Deed - A Corrective Deed prevents misunderstandings regarding property rights.

Understanding the importance of a Release of Liability form is essential for anyone participating in high-risk activities; it helps ensure that all parties are aware of the potential risks involved. Additionally, resources such as TopTemplates.info provide valuable information on how to properly utilize this legal document to safeguard against unexpected claims.

When filling out the Deed in Lieu of Foreclosure form, it is essential to approach the process with care and attention. Here are some important guidelines to follow, as well as some common pitfalls to avoid.

Following these guidelines can help ensure that your submission is accurate and complete, ultimately aiding in a smoother process. Remember, taking the time to do it right can make a significant difference in your experience.

Many homeowners facing financial difficulties may consider a deed in lieu of foreclosure as a solution. However, several misconceptions can cloud understanding of this option. Here are six common misconceptions:

Understanding these misconceptions can help homeowners make more informed decisions about their options when facing financial difficulties.

Once you have decided to proceed with a Deed in Lieu of Foreclosure, it’s important to carefully fill out the necessary form. This step is crucial as it helps ensure that you are taking the right legal steps to transfer ownership of your property back to the lender. After completing the form, you will typically submit it to your lender for review and further instructions on what happens next.